Relying on the supplier’s invoice price (Ex-Factory) to determine profitability is a critical oversight in global trade. True business viability depends on Landed Cost. This metric represents the total end-to-end expense required to transport a product from the manufacturer to the final destination, aggregating logistics, duties, taxes, and compliance fees.

This guide provides a comprehensive analysis of the landed cost anatomy, moving from component breakdown to calculation formulas and Incoterms® 2020 implications. It examines regional sourcing dynamics, specifically the opportunities and logistics challenges in Vietnam and outlines data-driven strategies for optimization, equipping businesses with the framework to protect profitability.

Contents

- 1 Introduction: The Strategic Importance of Landed Cost

- 2 Anatomy of Landed Cost: Key Components

- 3 The Mathematics of Profitability: Calculation Formulas

- 4 Regional Spotlight: Sourcing from Vietnam

- 5 Regulatory Framework: HTS Codes & Incoterms®

- 6 Strategies for Optimization and Automation

- 7 Conclusion: Mastering Unit Economics

Introduction: The Strategic Importance of Landed Cost

Landed cost represents the total expense required to transport a product from its origin to the final destination. This metric aggregates the initial product price with shipping fees, insurance, customs duties, taxes, handling fees, and currency conversion costs. Accurate calculation of landed cost determines business viability in international trade.

Accurate landed cost calculations ensure competitive pricing and flawless inventory valuation.

Companies in the e-commerce and B2B sectors rely on this data to determine true profitability and set competitive pricing strategies. Incorrect calculations result in direct financial risks. These risks include:

- Underpricing of products.

- Reduced profit margins.

- Inaccurate inventory valuation on balance sheets.

Product Price vs. Landed Cost

Buyers frequently confuse the Ex-Factory price (supplier’s price) with the total cost of goods sold. Under Incoterms® 2020 (ICC – International Chamber of Commerce) standards for Ex Works (EXW), the product price excludes all logistics and clearance costs.

Landed cost encompasses the complete supply chain expenditure. This includes freight, insurance, and variable costs such as demurrage fees or compliance testing. Accurate calculation prevents financial discrepancies.

Landed cost matters. Accurate calculation prevents financial discrepancies before they hit your bottom line.

Example: A product has a manufacturing cost of $10. A projected sale price of $25 suggests a $15 gross margin. However, logistics, tariffs (based on USITC rates), and handling fees may total $20 per unit. This results in a net loss of $5 per sale.

The Role of Product Validation

Product validation determines the financial and technical feasibility of sourcing. This process differs from marketing validation, which assesses consumer demand. Validation identifies regulatory requirements and cost structures prior to manufacturing. U.S. Customs and Border Protection (CBP) enforces strict compliance for specific categories.

From regulatory testing to cost structures, securing your product’s feasibility is the ultimate shield against unexpected supply chain bottlenecks.

- FDA: Required for food and health products.

- FCC: Required for electronics emitting radio frequencies.

Early identification of these requirements allows companies to calculate the total landed cost accurately. This data supports ” go/no-go ” investment decisions based on actual profit margins rather than estimated product costs.

Anatomy of Landed Cost: Key Components

Supply chain optimization requires a detailed breakdown of cost drivers. Landed cost comprises direct costs (commercial invoice) and indirect costs (logistics and risk management). Identifying these elements enables accurate calculation and cost reduction.

Direct Product & Manufacturing Costs

The direct product cost represents the supplier’s base price. This aligns with the Incoterms® 2020 definition of Ex Works (EXW), where the buyer assumes all costs after goods leave the factory.

True unit cost is revealed only when every hidden manufacturing variable is accounted for.

Companies manage this cost lever through negotiation terms and volume discounts. However, the invoice price is incomplete without accounting for fixed costs. Expenses such as specific tooling or molding fees must be amortized across the total production run. This calculation reflects the true unit economics.

Logistics, Freight, and Handling

Shipping expenses depend on the mode of transport (sea, air, rail, or road). Freight costs fluctuate based on distance, gross weight, and volumetric weight.

- Volumetric Weight: Carriers apply standards from the International Air Transport Association (IATA) to charge based on package dimensions rather than actual weight. This impacts bulky items significantly.

Size matters just as much as weight in logistics. Knowing how Chargeable Weight is calculated prevents surprise bills at checkout.

Supply chains also incur handling fees beyond the primary freight bill. Common charges include:

- Terminal Handling Charges (THC): Fees collected by terminal operators for container movement.

- Demurrage & Detention: The Federal Maritime Commission (FMC) defines these as penalty fees charged when containers exceed the allotted “free time” at terminals or depots.

- Inland Transportation: Costs for drayage or trucking from the port of entry to the destination warehouse.

Failure to incorporate these specific surcharges leads to underestimation of the total landed cost.

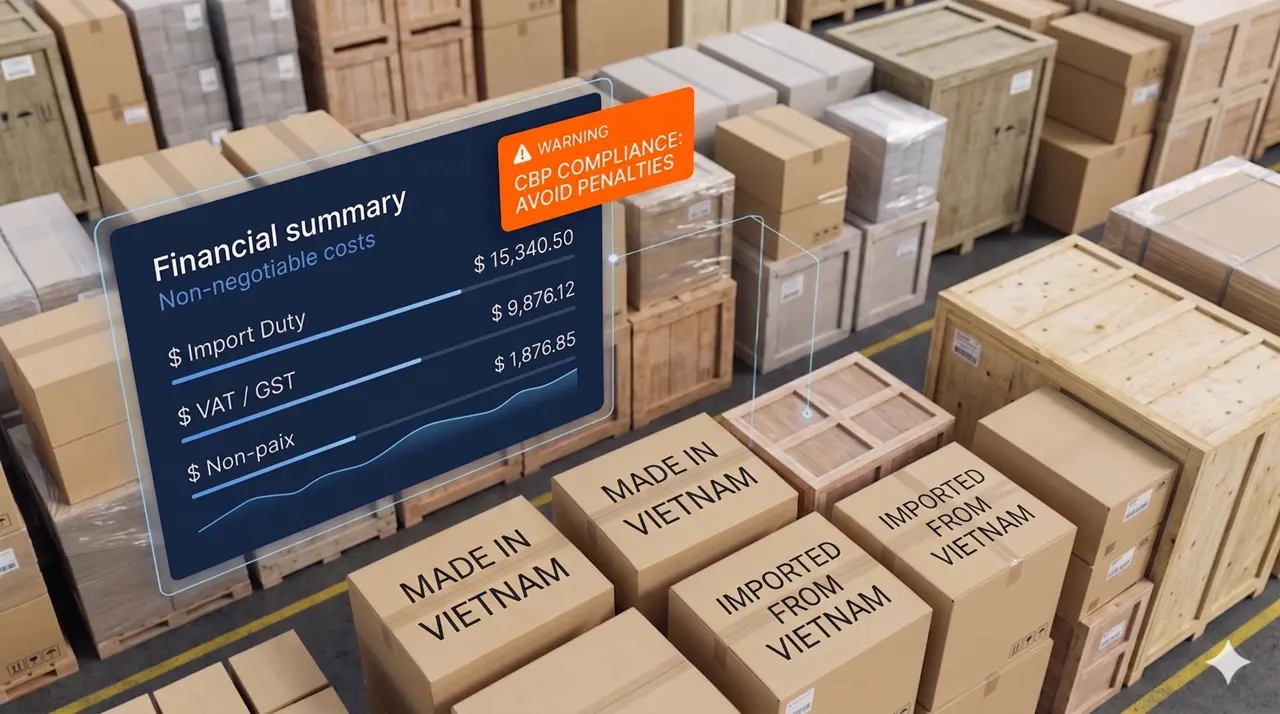

Customs, Duties, and Taxes

Customs duties function as non-negotiable fixed costs. Importing countries levy these tariffs based on the Harmonized System (HS) codes established by the World Customs Organization (WCO). The final duty rate depends on product classification, country of origin, and the declared value.

Geopolitical policies impact cost structures directly. For example, the Office of the United States Trade Representative (USTR) implemented Section 301 tariffs on specific Chinese goods, adding up to 25% to the standard duty rate.

Visualizing import duty structures and CBP compliance to secure profit margins and avoid non-negotiable financial penalties.

Importers must ensure accurate classification. U.S. Customs and Border Protection (CBP) enforces penalties and detainment for misclassified goods. Additionally, local taxes such as VAT or GST apply upon entry and must be included in the total cost calculation.

Risk Management & Miscellaneous

The final cost component involves risk mitigation and regulatory compliance. These expenses protect the investment and ensure market access.

- Cargo Insurance: Premiums depend on the goods’ value and coverage level. Under Incoterms® 2020, terms like CIF (Cost, Insurance, and Freight) mandate the seller to provide minimum insurance coverage.

- Compliance Certification: Regulated sectors incur costs for mandatory testing and labeling.

- European Chemicals Agency (ECHA): Requires REACH compliance for chemical substances entering the EU.

- Federal Agencies (USA): The FDA regulates food/drugs, while the FCC oversees electronic interference standards.

- Financial Fees: Currency exchange fluctuations and bank transfer charges affect final profit margins.

The Mathematics of Profitability: Calculation Formulas

Businesses must apply a standardized formula to determine the true unit cost. According to IRS guidelines for Cost of Goods Sold (COGS), inventory valuation includes the purchase price plus all direct costs incurred to acquire the goods.

The Basic Landed Cost Formula:

Landed Cost = Product Cost + Shipping/Freight + Customs Duties + Taxes + Insurance + Handling Fees + Miscellaneous Costs.

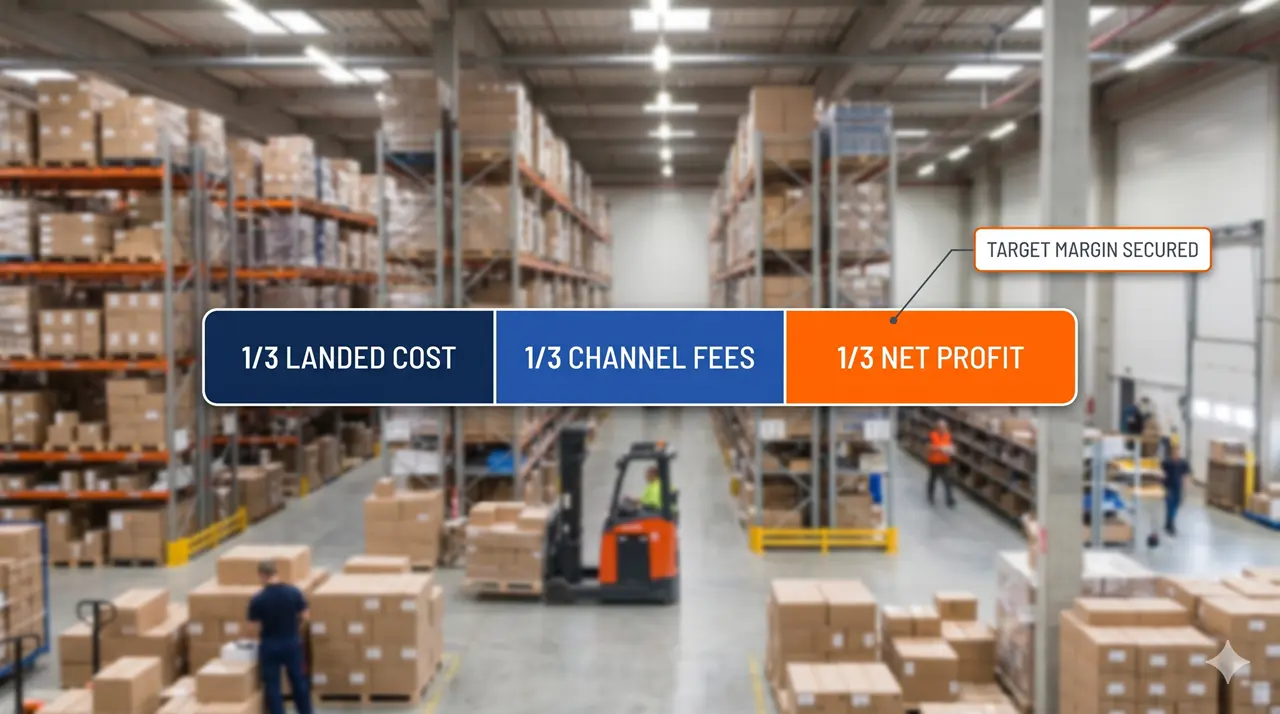

For initial feasibility assessments, e-commerce retailers often utilize the “Rule of Thirds” benchmark. This model allocates revenue into three segments:

- 1/3 for Landed Cost: Manufacturing and logistics.

- 1/3 for Channel Fees: Marketplace commissions (e.g., standard 15% referral fees on Amazon) and advertising.

- 1/3 for Net Profit: The target margin.

According to IRS guidelines for Cost of Goods Sold (COGS), your inventory valuation must integrate the purchase price with every single direct cost required to acquire those goods.

Calculation Methodology

Accurate calculation relies on specific data points rather than assumptions. The workflow involves three primary steps:

- Product & Freight Data: Obtain preliminary estimates from suppliers and freight forwarders. These figures provide the baseline Cost and Freight (CFR) value.

- Duty Determination: Locate the 10-digit Harmonized Tariff Schedule (HTS) code using the U.S. International Trade Commission (USITC) database. This determines the exact duty rate mandated by CBP.

- Unit Allocation: Sum all aggregate costs and divide by the total number of units.

This process transforms variable logistics data into a fixed per-unit cost, enabling precise margin analysis.

Case Study A: Standard General Import

This scenario models a shipment of 1,000 units from Vietnam to a U.S. fulfillment center.

Assumptions: Product cost is $10/unit; Sea freight rate is standard LCL (Less than Container Load).

Cost Breakdown (Per Unit):

- Product Cost (FOB): $10.00

- Freight & Insurance: $0.90

- Customs Duties (5%): $0.50

- Merchandise Processing Fee (MPF): $0.05 (Replaced generic VAT with specific US import fee)

- Port & Handling: $0.20

- Domestic Logistics: $0.25

- Total Landed Cost: $11.90

Without accurate data, that invisible cost directly erodes your bottom-line profit.

Impact Analysis: The final landed cost reflects a 19% increase over the FOB price of $10. A pricing strategy based solely on the $10 supplier quote would underestimate costs by $1.90 per unit, eroding margins by the same amount.

Case Study B: High-Volume Goods (Rattan Furniture)

Logistics costs scale disproportionately for bulky items with low value-to-volume ratios. This case involves importing Rattan Furniture (HS Code 9403.60) to the U.S. market.

Cost Breakdown (Per Unit):

- Ex-Factory Price: $50.00

- Sea Freight (Volume-based): $10.00 (20% of product value)

- Customs Duty (Free under certain FTAs, or Standard): $0.00 – $5.00 (Depending on GSP status). Let’s assume standard rate: $5.00

- Compliance Testing (CPSC Standards): $5.00

- Port & Drayage: $3.00

- Total Landed Cost: $73.00

Sea freight alone accounts for 20% of the product value here, and combined with compliance testing (CPSC Standards) and port drayage, the hidden expenses stack up fast.

Impact Analysis: The landed cost is 46% higher than the ex-factory price of $50. Freight and port handling together represent almost 20% of the total landed cost. For bulky, low value-to-volume products like rattan furniture, logistics efficiency and container utilization become the main drivers of profitability, often more material than small unit price reductions at the factory level.

Regional Spotlight: Sourcing from Vietnam

Vietnam functions as a primary manufacturing alternative to China, specifically for furniture, textiles, and electronics. While labor costs remain competitive, landed cost calculations must account for specific regional logistics and trade frameworks.

Vietnam-Specific Advantages

The European Commission confirms that the EU-Vietnam Free Trade Agreement (EVFTA) eliminates duties on 99% of tariff lines, offering a distinct margin advantage for European buyers.

By integrating these specific geopolitical incentives into your landed cost model, you maximize bottom-line returns.

For U.S. companies, Vietnam provides a “China Plus One” diversification strategy to mitigate Section 301 tariffs. Although no bilateral FTA exists (goods enter under Normal Trade Relations status), the absence of punitive tariffs usually results in a lower total landed cost compared to Chinese origins.

Regional Challenges & Considerations

Logistics efficiency remains a variable. According to the World Bank’s Logistics Performance Index (LPI), Vietnam ranks below major hubs like China or Singapore. This infrastructure gap often translates into higher inland trucking costs and longer transit times to ports.

Financial risks include currency fluctuation managed by the State Bank of Vietnam. Additionally, buyers must budget for third-party inspection services to bridge cultural and language gaps, ensuring quality control aligns with international standards.

Industry-Specific Examples

Landed cost drivers vary significantly by sector:

- Furniture (e.g., Plywood Cabinets): This category faces regulatory volatility. The U.S. Department of Commerce (DOC) imposes Anti-Dumping Duties (AD) on specific Vietnamese hardwood plywood derived from Chinese inputs. A base unit cost of $50 can incur an unexpected 200% duty if supply chain traceability is undocumented.

- Textiles: Compliance adds cost. Factories adhering to Better Work Vietnam (ILO) standards may charge premiums ($3.00 shirt landing at $5.00) to cover social compliance audits required by global brands.

Landed cost drivers vary significantly by sector, and regulatory volatility can change your unit economics overnight.

Regulatory Framework: HTS Codes & Incoterms®

Compliance operates alongside financial calculation as a pillar of landed cost. Under Customs Modernization Act (Mod Act) principles, the importer of record bears “reasonable care” responsibility for compliance, not the supplier.

Under Customs Modernization Act (Mod Act) principles, the responsibility for compliance does not fall on your supplier.

Harmonized Tariff Schedule (HTS)

U.S. Customs and Border Protection (CBP) applies duty rates based on the Harmonized Tariff Schedule. Importers must identify the correct 10-digit code using the U.S. International Trade Commission (USITC) database.

For unclassified products, relying on “similar items” is insufficient. The strategic approach involves requesting a Binding Ruling from CBP to guarantee duty certainty before shipment.

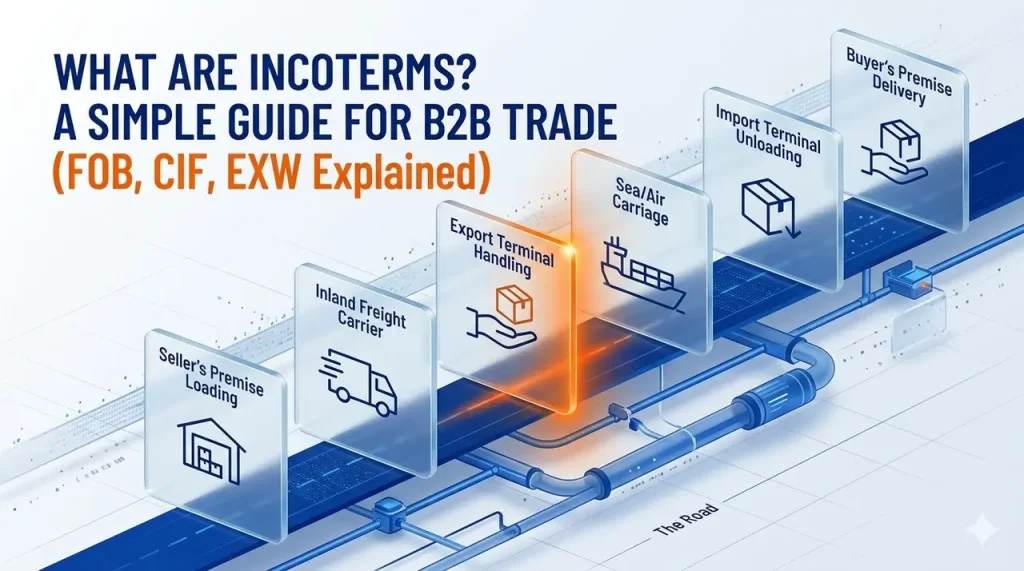

Incoterms® 2020 Definitions

The ICC establishes Incoterms rules to define cost and risk transfer. These terms directly impact the landed cost structure:

- FOB (Free On Board): The buyer assumes freight costs and risks from the port of origin. This term provides the buyer with maximum control over logistics vendors and rates.

- CIF (Cost, Insurance, Freight): The seller manages logistics to the destination port. While administratively simpler, this often includes hidden margins in the freight cost, inflating the final landed price.

- EXW (Ex Works): The buyer pays all costs from the factory floor. This offers the lowest invoice price but transfers maximum risk and logistics workload to the importer.

Balancing the invoice price against your internal logistics workload is key to picking the right framework.

Regulatory Agencies and Compliance

CBP enforces admissibility standards set by Partner Government Agencies (PGAs). Non-compliance results in shipment detainment or seizure.

- FDA (Food & Drug Administration): Regulates consumables and medical devices under 21 CFR.

- FCC (Federal Communications Commission): Mandates certification for radio-frequency devices (Bluetooth, Wi-Fi) prior to importation.

- USDA (Dept. of Agriculture): Enforces APHIS permits for agricultural/wood products to prevent invasive species.

Strategies for Optimization and Automation

Optimization of landed cost directly improves net profit margins independent of retail pricing. Scaling operations requires a shift from manual estimation to automated systems.

Cost Reduction Strategies

- Incoterm Negotiation: Shifting terms from CIF to FOB allows buyers to control freight selection, often reducing costs by leveraging competitive bidding among forwarders.

- Consolidation (LCL to FCL): Logistics data indicates that Less than Container Load (LCL) shipments incur higher per-unit costs due to handling surcharges. Consolidating orders into Full Container Loads (FCL) improves container utilization.

- Design Efficiency: Optimizing packaging for higher “Fill Rates” reduces shipping air. Strategies like flat-packing (popularized by IKEA) maximize cubic meter (CBM) usage, effectively lowering freight cost per unit.

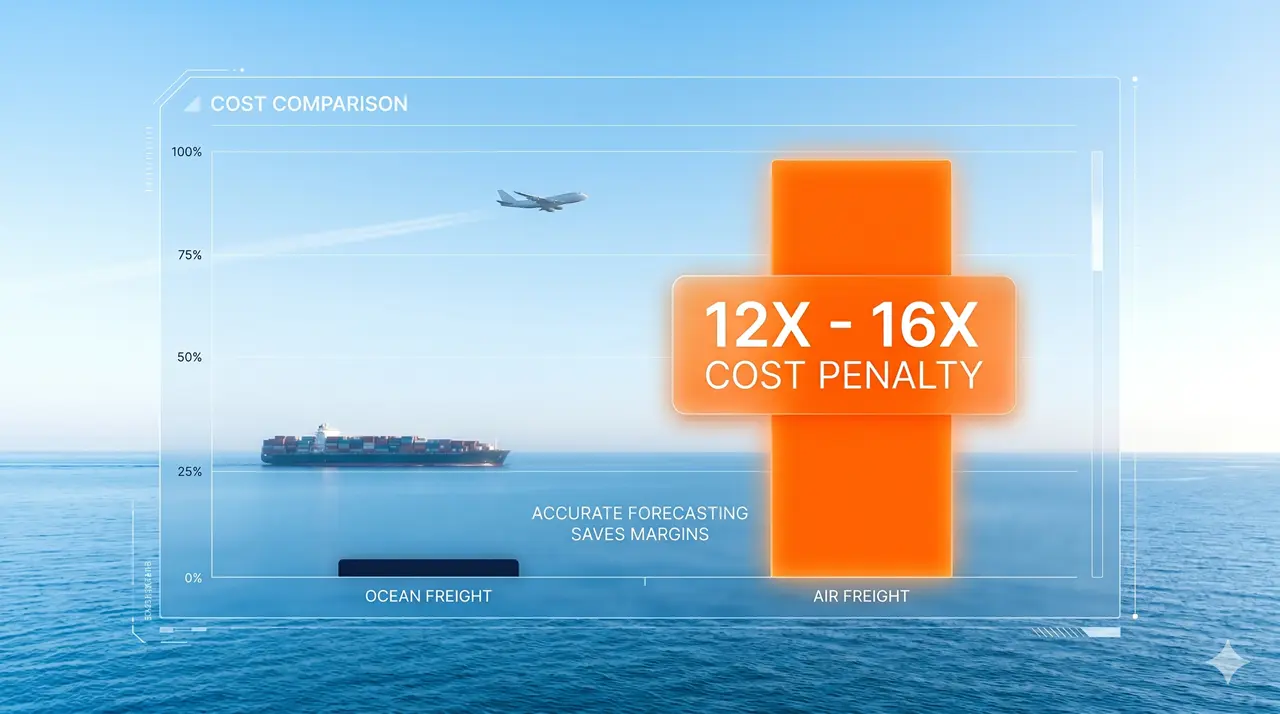

- Inventory Planning: Accurate demand forecasting prevents stockouts, eliminating the need for emergency air freight. According to World Bank logistics data, air transport costs are significantly higher than ocean freight, typically ranging from 12 to 16 times more per unit of weight.

Visualizing the air vs. ocean freight cost gap: Accurate demand forecasting is critical to avoiding emergency air freight penalties of 12x–16x and securing long-term profit margins.

Leveraging Technology

Manual spreadsheet calculations are prone to human error. Modern supply chains utilize Landed Cost Engines integrated within ERP systems to automate this process.

- Scenario Planning: Leveraging Supply Chain Digital Twin technology (a concept endorsed by Gartner), businesses simulate variables, such as shifting sourcing from China to Vietnam, to forecast the total landed cost impact before capital commitment.

- Real-time Data Integration: Integration with Transportation Management Systems (TMS) automates the capture of live freight and currency rates. This connectivity facilitates Variance Analysis, allowing finance teams to audit the delta between estimated standard costs and actual invoiced costs.

Conclusion: Mastering Unit Economics

Profitability in international trade depends on the precision of cost management, not merely the negotiation of product prices. A comprehensive landed cost strategy integrates financial calculation with regulatory compliance and logistics optimization.

Companies must move beyond manual estimation. The application of Incoterms® 2020 for risk allocation, the accurate classification of HTS codes for duty determination, and the utilization of Supply Chain Planning software are essential requirements for scaling operations.

By controlling these variables, businesses mitigate the risks associated with volatile freight rates and tariff changes. Ultimately, the ability to calculate and optimize total landed costs ensures that sourcing initiatives contribute directly to the net profit margin rather than becoming a financial liability.