Digital commerce has evolved from a supplementary sales channel into the primary engine of global business strategy. Whether facilitating complex enterprise procurement or capturing individual consumer demand, the choice of business model – B2B, B2C, or hybrid variations like D2C – dictates operational architecture and financial viability.

While these models increasingly share technological infrastructure, they require distinct execution playbooks regarding customer acquisition, pricing logic, and retention mechanics. This article analyzes the structural nuances of these ecosystems, evaluating how converging buyer expectations and emerging data strategies are reshaping the fundamental rules of trade.

Contents

Core Business Models and Classifications

Global commerce utilizes specific business models driven by market data. In 2023, global retail e-commerce sales reached $5.8 trillion with projections suggesting a surge to over $8 trillion by 2027 (Source: Statista). Companies must distinguish between serving businesses and consumers to align operational strategies with revenue goals.

B2B (Business-to-Business)

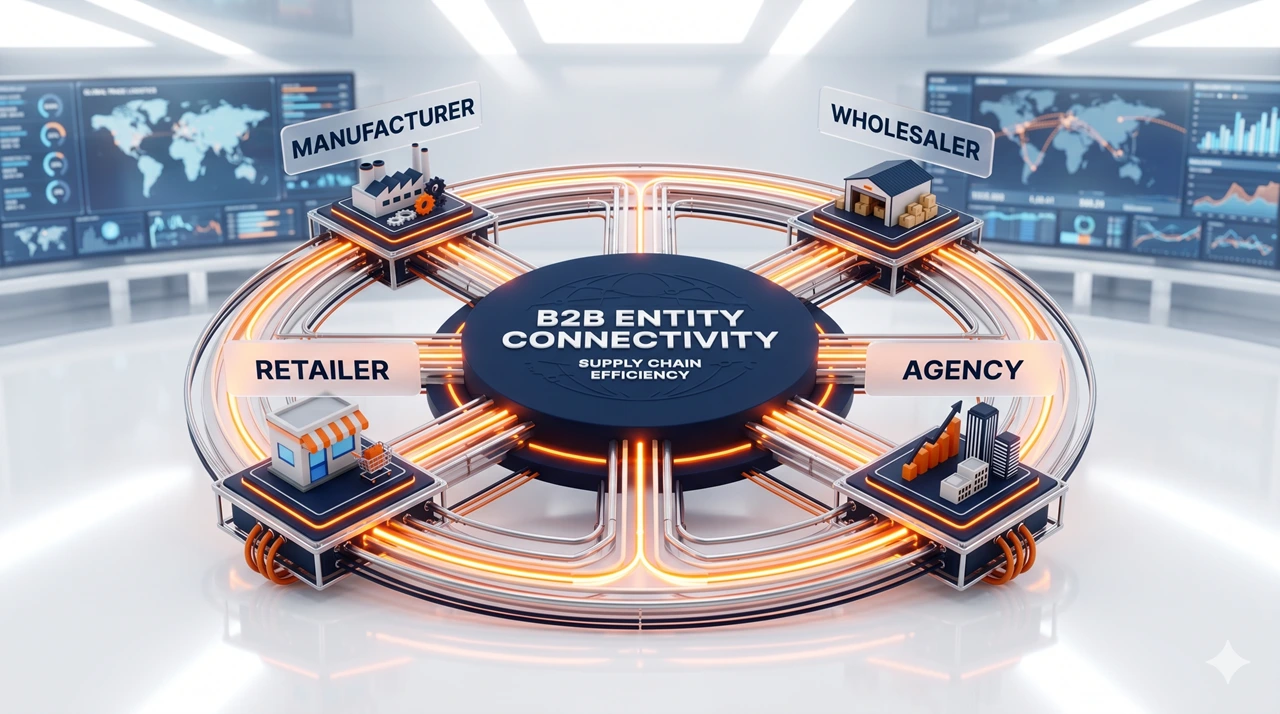

B2B e-commerce consists of transactions between business entities, including manufacturers, wholesalers, agencies, and retailers. According to Grand View Research, the global B2B e-commerce market size was projected to reach USD 57,578.97 billion by 2030, with a CAGR of 18.2% from 2024 to 2030. This indicates a significant growth trajectory for the B2B e-commerce sector, driven by digital transformation and the increasing preference for efficient purchase processes.

Integrated B2B entity connectivity streamlines operations between manufacturers, wholesalers, and retailers to maximize supply chain efficiency.

Unlike consumer-facing models, B2B prioritizes efficiency, logic, and operational requirements. The decision-making process involves the following characteristics:

- Bulk Transactions: Buyers purchase high volumes for inventory, dropshiping, or private label purposes.

- Complex Infrastructure: Systems must handle intricate logistics, credit terms, and tiered pricing.

- Logic-Driven Decisions: Purchases focus on profit margins and supply chain efficiency rather than emotion.

B2C (Business-to-Consumer) and Models

B2C e-commerce involves businesses selling products directly to individual consumers. Companies like Amazon, Newegg, and Target lead this sector through high-volume transaction models and optimized logistics. Within B2C, distinct operational sub-models exist to address specific market needs.

Direct-to-Consumer (D2C)

D2C brands bypass intermediaries (wholesalers and retailers) to sell directly to end users. According to eMarketer, US D2C e-commerce sales are projected to reach $212.9 billion in 2024, reflecting a shift toward brand independence.

The D2C model bypasses traditional intermediaries to offer brands higher margins and direct consumer relationships.

Examples include Gymshark, Warby Parker, and Casper. This model presents a specific financial structure:

- Margin Control: Companies retain full profit margins by eliminating retailer markups.

- Data Ownership: Brands possess direct access to customer purchasing data for personalization.

- Cost Impact: The absence of retail partners transfers all marketing and infrastructure costs to the brand, typically resulting in a higher Customer Acquisition Cost (CAC).

Dropshipping

In the dropshipping model, retailers sell products sourced from third-party suppliers without holding physical inventory. Grand View Research valued the global dropshipping market at $225.99 billion in 2022, driven by its capital efficiency.

The dropshipping model eliminates inventory risk by allowing suppliers to fulfill orders directly to end customers.

Retailers like Fresh Juice Blender use this model to minimize upfront capital risk and warehousing costs. However, companies must navigate specific operational constraints:

- Slim Margins: Competition is high, and product differentiation is low.

- Fulfillment Control: Retailers rely entirely on suppliers for shipping speed and product quality.

- Success Factor: Profitability depends heavily on marketing efficiency and customer service rather than product exclusivity.

Subscription-Based

This model generates revenue through recurring product delivery, focusing on maximizing Customer Lifetime Value (LTV). According to Juniper Research, the global subscription e-commerce market is projected to reach $275 billion by 2026.

The subscription model drives sustainable growth by maximizing Customer Lifetime Value (LTV) through a recurring revenue cycle.

Brands like Blue Apron and Dollar Shave Club utilize this strategy to secure predictable cash flow. Implementation requires specific operational capabilities:

- Tech Infrastructure: Systems must support automated recurring billing (e.g., WooCommerce Subscriptions).

- Logistics Precision: Supply chains must ensure timely delivery to maintain customer satisfaction and prevent churn.

- Retention Focus: Profitability relies on extending the subscription duration rather than one-time sales.

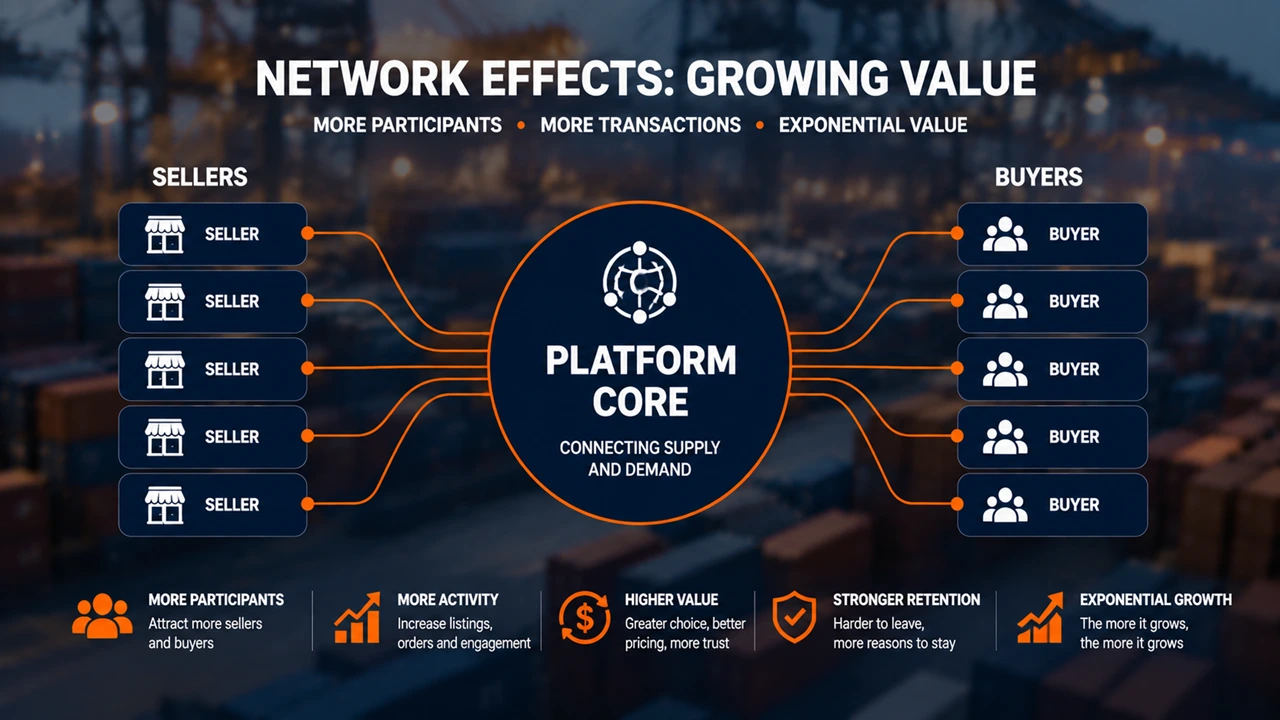

Marketplace Model

Marketplaces act as centralized platforms connecting third-party sellers with buyers. This model dominates global e-commerce; data from Digital Commerce 360 indicates that the top 100 marketplaces accounted for over 60% of global online retail sales in 2022.

The marketplace model leverages network effects to drive exponential growth by connecting supply and demand through a central platform core

Platforms like Amazon and Etsy monetize this volume through transaction fees, listing charges, or advertising. The model operates on the following principles:

- Network Effects: The platform’s value increases as more users (buyers and sellers) participate.

- Scalability: Operators do not hold inventory but must manage high traffic volumes.

- Revenue Streams: Income is derived from commissions rather than product margins.

Alternative and Hybrid Classifications

Beyond traditional B2B and B2C structures, hybrid models have emerged to maximize asset utilization and address specific market gaps.

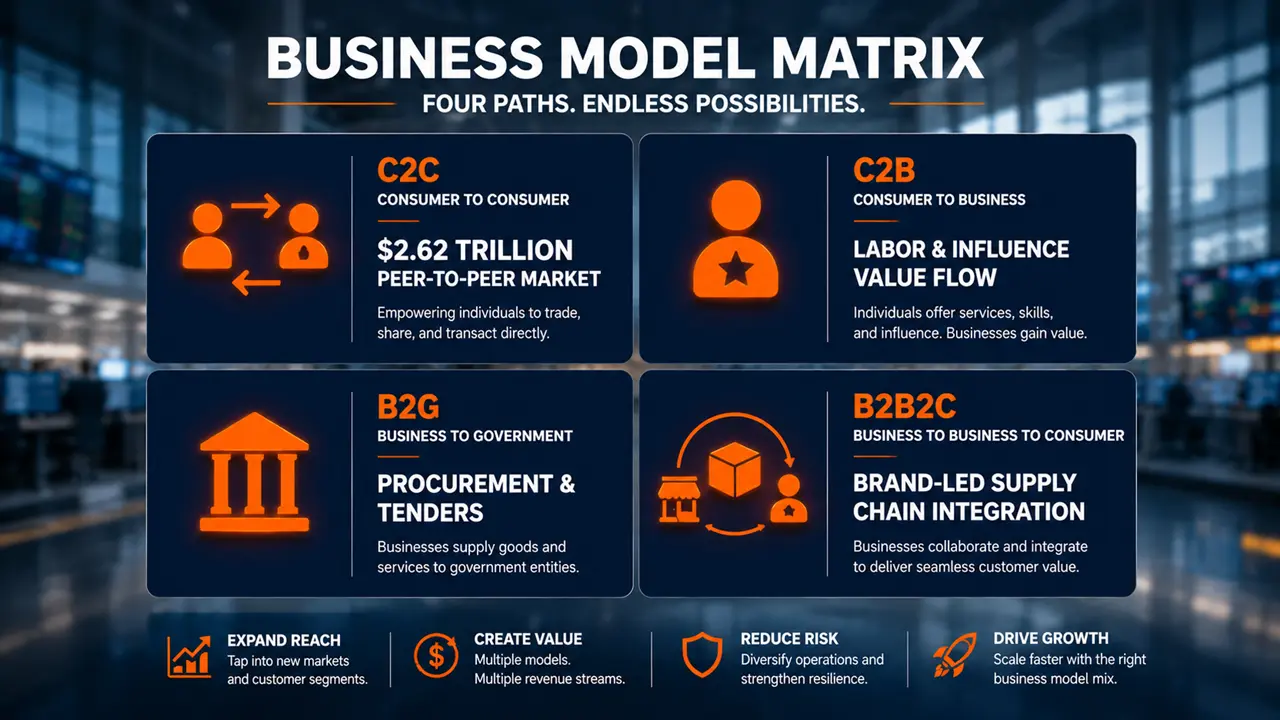

The business model matrix highlights strategic paths like B2B2C and C2B to expand market reach and drive long-term growth.

- C2C (Consumer-to-Consumer): Platforms like eBay or Upwork facilitate direct exchanges between individuals. According to Grand View Research, the global C2C market was valued at $2.62 trillion in 2023. These platforms monetize trust and liquidity through transaction fees rather than inventory ownership.

- C2B (Consumer-to-Business): In this model, individuals sell value, such as labor or influence, to businesses. Competitive advantage in this sector relies on agile pricing and specialized skill access.

- B2G (Business-to-Government): This sector involves firms selling directly to government agencies. Success requires strict adherence to procurement regulations and the management of long tender processes.

- B2B2C (Business-to-Business-to-Consumer): Manufacturers align with distributors to reach consumers while retaining control over branding and data. Unlike traditional distribution, this model integrates the supply chain digitally. Manufacturers originate sales and capture user data, while partners handle fulfillment. This approach mitigates channel conflict and improves customer lifetime value.

Strategic Comparative Analysis: B2B vs. B2C

B2B and B2C models require distinct strategies due to differing customer journeys. However, buyer expectations regarding digital experience are converging. According to the Sana Commerce B2B Buyer Report, 87% of B2B buyers are willing to switch suppliers for a better online experience. This data confirms that user experience is a critical competitive factor across both sectors.

Marketing Strategy and Audience

The audience size and motivation dictate the marketing approach.

| Feature | B2B Marketing Strategy | B2C Marketing Strategy |

| Target Audience | Narrow professional demographic (business owners, purchasing managers). Focuses on solving operational efficiency problems. | Broad demographic of individual consumers. Focuses on fulfilling personal desires or lifestyle needs. |

| Decision Making | Logic-driven. Research from Gartner indicates a typical buying group involves 6 to 10 decision-makers, requiring consensus. | Emotion-driven. Purchases are often impulsive or based on immediate gratification. |

| Content Focus | Technical and solution-oriented (e.g., whitepapers, case studies). Aims to demonstrate long-term value and ROI. | Experiential and visual. Uses lifestyle imagery and simplified messaging to trigger quick, direct sales. |

Buying Behavior and Decision Making

Understanding the “how” and “why” of the purchase is critical for conversion optimization.

| Feature | B2B Marketing Strategy | B2C Marketing Strategy |

| Method of Buying | Collaborative. Involves complex processes with multiple departments (finance, operations, management) and stakeholders. | Solitary. Individuals make independent decisions based on personal needs. |

| Sales Cycle | Long. Requires nurturing and persistence. The process is research-heavy with multi-layered approval steps. | Short. often measured in minutes or days. Decisions are frequently driven by immediate needs or impulse. |

| Primary Driver | Logic & Data. Decisions are based on business mandates, statistics, and efficiency metrics. | Emotion. Decisions are driven by feelings. “Impulse buying” is a significant revenue driver. |

Pricing, Branding, and Design

B2B strategies prioritize utility and negotiated value for high-stakes transactions, whereas B2C strategies focus on visual appeal and transparent pricing to drive volume.

| Feature | B2B Marketing Strategy | B2C Marketing Strategy |

| Pricing Structure | Complex & Negotiable. High order values (often >$10,000). Pricing is variable based on volume and contract terms. | Fixed & Transparent. Lower transaction values (typically 100 – 200). Pricing is standard with no negotiation. |

| Branding Style | Sophisticated. Prioritizes minimalism, professionalism, and stability to appeal to corporate buyers. | Vibrant. Uses novelty, niche appeal, and high energy to stand out in a crowded market. |

| Website UX/UI | Utility-First. Focuses on detailed specs, comparison tables, and access to sales teams (live chat). | Visual-First. Focuses on high-quality product imagery and lifestyle context. Uses chatbots for basic FAQs. |

Despite these differences, the gap is closing. Both sectors increasingly demand a “modern buying experience.”

| Element | Strategic Impact on Both Sectors |

| Digital Self-Service | Both buyer types demand simple ordering, personalized content, and user-friendly design. A consistent brand experience across channels is a baseline requirement. |

| Multichannel Engagement | Decision-makers in both sectors rely on digital channels (LinkedIn, Facebook, Twitter). Forrester research indicates that 59% of buyers prefer online research over speaking to a salesperson. |

| Psychological Drivers | Despite different motivations, all buyers respond to core psychological principles, such as the fear of loss (FOMO) or the desire for status/benefits. |

Operational Workflows and Platform Architecture

Platform architecture dictates operational scalability. B2B and B2C models differ significantly in complexity, specifically regarding integration requirements. B2B platforms require account hierarchies and approval workflows to match client organizational structures, whereas B2C platforms prioritize transaction speed and simplicity.

Buyer Journey Operational Differences

| Feature | B2B Operational Reality | B2C Operational Reality |

| Registration | Verification Required. Acts as a gatekeeper to verify business credentials and align contracts. | Frictionless. Barriers are minimized via instant sign-up or guest checkout to prevent abandonment. |

| Browsing | Restricted. Displays personalized catalogs and negotiated pricing only after login. | Open. Displays full catalogs with standard retail prices to all visitors. |

| Ordering | Complex. Supports bulk quantities, Purchase Orders (POs), and multi-level approval chains. | Linear. Follows a standard path: Add to cart -> Apply codes -> Checkout. |

| Checkout | Term-Based. Supports invoicing, net terms (e.g., Net 30), and credit limits. | Instant Settlement. Relies on credit cards, digital wallets, or BNPL services. |

| Post-sale | Relationship-Heavy. Focuses on contract compliance and dedicated account management. | Transactional. Focuses on automated promotions and retargeting ads. |

Platform Selection and Integration Architecture

| Criteria | B2B Requirements | B2C Requirements |

| Scalability | Complexity Focus. Must handle intricate SKU variations and bulk order processing. | Volume Focus. Must be elastic to handle massive traffic spikes during peak demand. |

| Integration Priority | Backend Efficiency. Deep integration with ERP, CRM, and procurement systems (e.g., SAP, Microsoft Dynamics). | Frontend Agility. Integration with marketing tools, shipping logistics, and payment gateways. |

| Analytics Goal | Client Health. Tracks account-based sales, invoice monitoring, and credit utilization. | Conversion ROI. Tracks traffic sources, bounce rates, and advertising return on investment. |

Standardizing B2B Experience (B2C-ification)

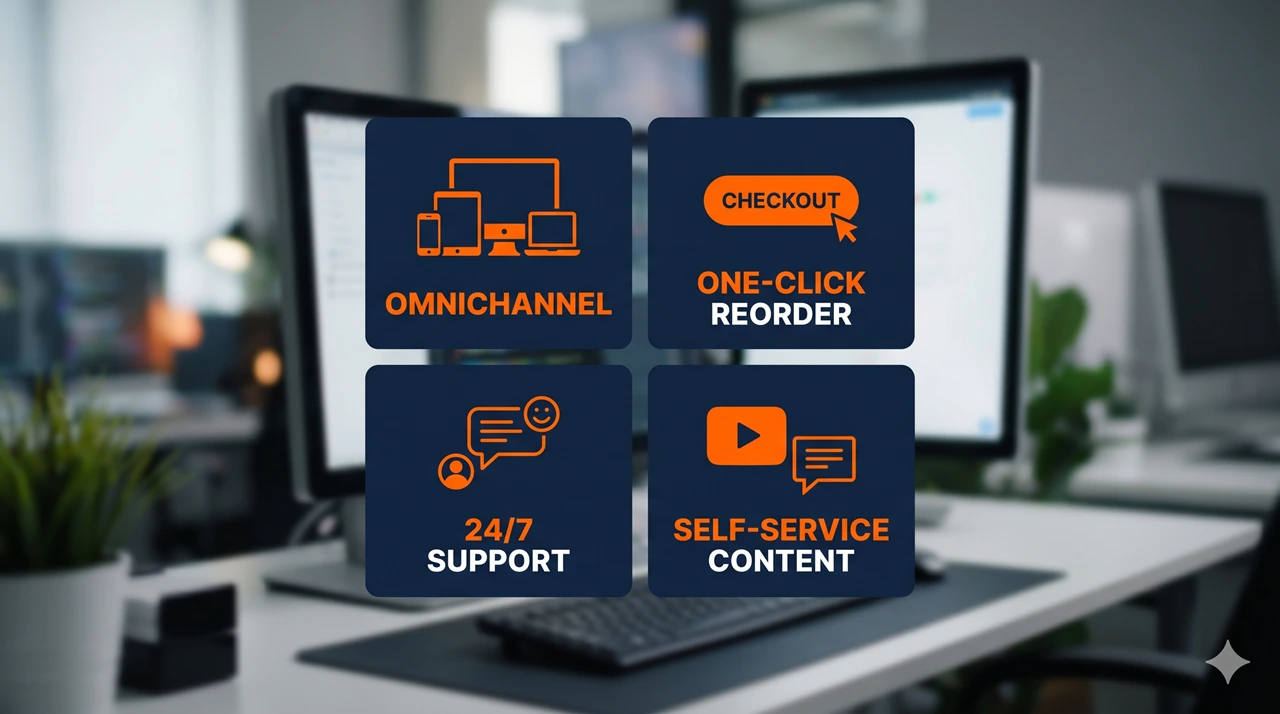

B2B platforms must adopt B2C usability standards to remain competitive.

Adopting B2C usability standards like omnichannel support and self-service content is essential for standardizing the modern B2B experience.

- Seamless Omnichannel Experience: According to Salesforce, 75% of buyers expect connected processes across devices and touchpoints. Consistency builds trust.

- Streamlined Checkout: Friction reduction is critical. Research from Gartner indicates that only 15% of buyers prefer speaking to a sales representative for reorders. Implementing one-click reordering and subscription options directly addresses this preference.

- Customer Support: Implementing 24/7 chatbots and comprehensive FAQs reduces the administrative burden on sales teams.

- Content: Self-service resources, such as video demos and community forums, empower buyers and accelerate the research phase.

Sales and Marketing Funnels

The sales funnel structure determines how businesses capture value. While both models utilize the AIDA framework (Awareness, Interest, Desire, Action), the tactics differ significantly due to contrasting buyer motivations.

Marketing Funnel (AIDA) Strategic Comparison

| Criteria | B2B Tactics | B2C Tactics |

| Awareness | Solution-Seeking. Targets professionals actively searching for business solutions via SEO and technical content. | Lifestyle-Oriented. Targets consumers through social media and paid ads focused on lifestyle improvements. |

| Interest | Lead Generation. Captures contact info by offering high-value resources. Content Marketing Institute notes that whitepapers are among the most effective B2B lead magnets. | Immediate Incentive. Captures interest through discount codes or flash sale popups to trigger engagement. |

| Desire | Rational Proof. Built through product demos, case studies, and ROI calculators. | Social Proof. Driven by user-generated content and reviews. Research from Spiegel Research Center indicates reviews can boost conversion rates by 270%. |

| Action | Formal Process. Involves contracts, bank wires, and invoicing. | Instant Transaction. Utilizes card payments, digital wallets, and impulse upsells at checkout. |

Comparative Sales Funnel Dynamics

| Funnel Stage | B2B Strategy (High Touch) | B2C Strategy (High Velocity) |

| Acquisition (Awareness & Interest) | Authority First. Generates leads by sharing valuable insights, market reports, and free resources (eBooks) to establish expertise. | Impact First. Sparks immediate interest through arresting visuals, social media ads, and compelling website copy. |

| Evaluation (Consideration) | Logic Support. Aids internal decision-making with detailed quotes, pros/cons analyses, and competitive comparison articles. | Desire Building. Nurtures high-ticket buyers via email or evokes immediate desire through emotional copy and simplified landing pages. |

| Conversion (Intent & Sale) | Human Interaction. Involves direct engagement from sales teams for demos, sample orders, and contract negotiation. | Frictionless Transaction. Completes the sale instantly with minimal steps. This is the primary window for impulse upsells. |

| Retention (Post-Sale) | Interval-Based. Uses automated campaigns to prompt reordering for replenishable items, maximizing Customer Lifetime Value (LTV). | Frequency-Based. Leverages SMS and email marketing to drive repeat purchase frequency and brand loyalty. |

Market Trends and Emerging Ecosystems

The e-commerce sector is shifting toward system integration and data independence. Two primary shifts are redefining the landscape: the adoption of Unified Commerce and the expansion of B2B Marketplaces.

Current Strategic Trends

- Unified Commerce: Organizations are replacing disjointed systems with single platforms that manage all sales and operations (e.g., Shopify). According to Adyen, this consolidation results in a 60% reduction in maintenance costs and an 8.9% increase in Gross Merchandise Value (GMV).

- First-Party Data: Following the deprecation of third-party cookies, data ownership is critical. Brands now prioritize direct data collection, such as purchase history and browsing behavior, to drive personalization and lead capture.

- Data Cooperatives: To mitigate rising acquisition costs, independent merchants are joining cooperatives to pool anonymized data. McKinsey analysis suggests that leveraging such collective intelligence can reduce customer acquisition costs by up to 50%.

B2B Marketplaces

The digitization of wholesale is creating large-scale aggregators. Precedence Research predicts the global B2B e-commerce market will reach $60.62 trillion by 2034, with marketplaces serving as central hubs.

Marketplace Classifications and Revenue Models: These platforms monetize via commission fees, subscriptions for premium features, listing fees, and sponsored advertising.

| Marketplace Type | Strategic Focus | Examples |

| Wholesale | Focuses on bulk orders and discounted pricing for high-volume buyers. | Alibaba.com |

| Vertical (Industry-Specific) | Specialized platforms for niche sectors like healthcare, construction, or chemicals. | Medcart, CheMondis |

| Procurement | Streamlines complex purchasing and compliance processes for large enterprises. | SAP Ariba |

| Supply Chain | Connects businesses directly with distributors and logistics providers. | Flexport |

| Horizontal | Sells a wide range of goods across multiple categories to diverse business buyers. | Amazon Business |

Strategic Transitions: B2B to D2C

Manufacturers and wholesalers are increasingly adopting D2C strategies to bypass intermediaries. According to a report by Barclays Corporate Banking, 73% of manufacturers now sell directly to consumers. This shift allows companies to capture retail margins and control the customer experience, though it introduces the risk of channel conflict with existing partners.

Decision Factors: D2C vs. Third-Party Channels

| Factor | D2C Strategy (Owned Channel) | Third-Party/Marketplace Strategy |

| Product Fit | Niche/Unique. Best for products requiring detailed brand storytelling or education. | Commodity. Best for standard products where high traffic volume drives sales. |

| Financials | High Margin / High CAC. Removes retailer markups but requires heavy investment in infrastructure and traffic acquisition. | Lower Margin / Low CAC. Involves commission fees or wholesale discounts, but leverages existing traffic. |

| Data Control | Full Ownership. Grants direct access to first-party data for deep personalization and agility. | Restricted. Data belongs to the platform; brands receive limited customer insights. |

| Speed to Market | Slow Build. Requires time to build brand equity and organic traffic. | Rapid Scale. Allows for immediate access to a vast active user base. |

Implementation Strategy

Executing this transition requires a structured roadmap: Market Research > Digital Ecosystem Build > Launch > Optimization. Success is measured by KPIs such as Customer Acquisition Cost (CAC), Net Promoter Score (NPS), and Lifetime Value (LTV).

Mitigation of Channel Conflict

To avoid alienating retail partners, manufacturers should adopt a collaborative approach:

- Data Sharing: Sharing consumer insights with distributors improves the overall supply chain efficiency.

- Headless Commerce: Using headless solutions allows brands to innovate the customer experience on the frontend without disrupting backend distributor integrations.

Hybrid Models

The most resilient strategy is often a hybrid approach. Brands like Nike effectively blend direct sales with retail partnerships. This allows them to expand their D2C footprint (Nike Direct) for higher margins while maintaining the extensive market reach provided by wholesale partners. As Rick Wilson, CEO of Miva, states, “Selling B2B, B2C, and DTC on a single website is becoming the new norm.”

Conclusion

The rigid binary between B2B and B2C models is dissolving in favor of integrated, data-driven ecosystems. While the operational realities differ, with B2B requiring complex logic and B2C prioritizing speed, the strategic mandate for both is now identical: delivering a seamless, modern buying experience.

Market data confirms that the future belongs to Unified Commerce. The shift toward first-party data ownership, the expansion of B2B marketplaces to a projected $60.62 trillion, and the adoption of hybrid D2C strategies demonstrate that flexibility is the new currency of growth. Companies that successfully blend the operational efficiency of wholesale with the user-centricity of retail will secure a sustainable competitive advantage. Ultimately, success lies not in choosing between B2B or B2C, but in constructing an adaptable infrastructure capable of serving the customer at every touchpoint.